June 27, 2018

The common wisdom of the investing world is that as you age, your risk tolerance should diminish. After all, you don’t have as much time to make up for investment losses that will come around every so often. The advisory and investment products industries have done a thorough job of selling the idea that these periodic losses can’t be avoided, that diversification among different asset classes will sufficiently lower your losses and that you should always be invested. This business model has been great for them and periodically not so great for investors. For investors either in or nearing retirement, this business model is very dangerous.

My June 2018 copy of Financial Planning Magazine came with a full-page advertisement glued to the cover. Franklin Templeton Investments’ words “Reach for Better”, a marketing campaign, are emblazoned across the image of a person reaching for the sky while looking through virtual reality glasses. Their Reach for Better campaign is displayed prominently on their website, where they invite you to read a paper entitled “What Matters Most, The Case For Active Risk Management”. It starts off promisingly by pointing out that an investor’s first priority is usually to not lose their money. They then go on to point out that indexes are indifferent to bubbles, it’s important to reduce downside risk, volatility is bad for retirees and active management is the answer. After all, over 80% of Franklin Templeton funds’ holdings are deemed to be “active”. At Franklin, active management means stock picking and asset allocation, long only.

It seems obvious that Franklin believes that long-only, buy and hold passive investing (today’s predominant approach) is not a good idea for retirees. As I read the article it became evident why one would have to be peering through virtual reality glasses to think that the kind of active management being suggested would be expected to make “reaching for better” turn out to be actually better. For instance:

- Managing downside risk is defined as not losing as much as the entire market does during bad times;

- Franklin points out that a person with a $100,000 account and making 5% annual withdrawals who has a 40% drawdown in a market correction will have to make a 186% return to recover their initial loss.

Looking at the Franklin funds that have been in existence long enough to show performance through the last two major market corrections (2000 and 2008), you will see that most have had maximum drawdowns (and general downside volatility[1]) as bad or worse than the aggregate stock market, and they did not generally recover any faster. I guess this explains the need for the virtual reality glasses.

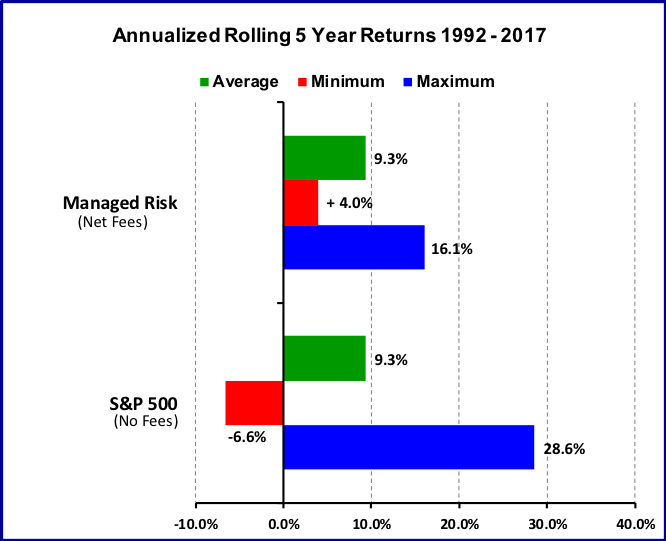

The non-virtual reality is that the way to avoid losing money is to embrace the kind of active management that will take you out of the market entirely when it is called for. This can be done by focusing on asset classes that lend themselves well to trend following and applying non-emotional, quantitative analysis to inform market entry and exit points. If you want to reach for better investing seek out a tried and proven absolute return strategy.

Trendhaven manages an absolute return strategy in separate accounts. www.trendhaven.net

See Ulcer Index: http://www.tangotools.com/ui/ui.htm